Davis was one of the remarkably few people who made a sizable fortune from investments in common stocks, serving as an inspiration to the ‘Average Joe’ that he too could become rich without resorting to shady shenanigans.

During the mid-1930s, the American stock market came under heavy selling pressure, striking terror into the hearts of investors who had just a few years back witnessed the Great Crash of 1929. Davis, who was running an investment firm then, began seeing an exodus of nervous clients.

Seeking to shore up the confidence of investors as well as his own staff, he asked his employees to prepare a list of everyone they knew who had wealth and then see how it had been acquired. The objective was to learn from the experiences of other investors and develop a long-term, fundamental philosophy of investment.

Hundreds of examples were turned in. Excluding the cases where wealth had been acquired through marriage or inheritance, the others fell in two categories—nine out of ten of the rich had made their fortune because they had been long-term stockholders in a successful enterprise; the small balance because they had ample cash (and courage) to buy stocks during a bear market.

View Full Image

For the larger group, the question arose as to why they did not sell even when they could have made a handy profit or capped their losses during a downturn.

Three main reasons were identified. First, they were not looking to time the market, that is they did not sell when their shares looked overpriced in the hope of buying them back later.

The second reason—and a pretty revealing one for market participants—was that some also had inside information about companies and knew beforehand of various promising corporate developments.

But it is the third reason which perhaps will be the most relevant for Indian investors, especially at this juncture. It was capital gains tax, which fortuitously locked the shareholders into not selling their quality stocks, ultimately bringing them a windfall.

Taxing Times

Grief, Hollywood superstar Keanu Reeves once said, changes shape, but it never ends.

The same can be said about taxation.

If you are a middle-class Indian, it can be hard to shake the feeling that our entire cosmic purpose in life is to pay taxes and die. The Union Budget 2024 did little to assuage these fears, especially for equity investors.

View Full Image

While the hike in short-term capital gains (STCG) as well as the securities transaction tax on futures and options (F&O) could be seen as necessary measures to curb the excesses in some segments of the market, what rankled most was the increase in long-term capital gains (LTCG) tax on the sale of listed equity shares and equity-oriented mutual funds from 10% to 12.5%.

More worryingly, the frequent revisions to the capital gains framework are sparking fears that the tax rates will be raised periodically over the next few years.

“The potential hike in STCG and LTCG taxes could significantly impact investor returns, potentially moving towards a European model with a common tax rate for stock gains,” Puneet Sharma, chief executive officer (CEO) and fund manager at Whitespace Alpha, an asset management firm, toldMint.

However, this does not mean investors should sink into a morass of melancholy.

Investing in AIFs could be considered, as their potential for higher growth might help offset increased tax burdens.

—Puneet Sharma

“While this shift may occur gradually, investors should consider strategies to mitigate the impact. These include focusing on tax-efficient investments such as ELSS funds, which offer benefits under Section 80C, adjusting holding periods to optimize tax liabilities, and diversifying across asset classes and geographies to spread risk.

“Additionally, investing in Alternative Investment Funds (AIFs) could be considered, as their potential for higher growth might help offset increased tax burdens,” he added.

Similarly, the removal of indexation benefit on property sales induced a collective groan from real estate investors, particularly those looking to sell older houses as they could be staring at a huge jump in their tax bill.

But barring these cases, there could be a silver lining for the overall financial services sector.

“Taking away the indexation perks in real estate, which let people adjust the purchase price for inflation, could push investors to look at other options like stocks and bonds. This change might make the market more liquid, help people spread out their investments, and boost the economy,” said Ravi Singh, senior vice president, retail research, Religare Broking.

“Stocks can bring in more money, while tax-free bonds give steady returns with less tax to pay. Other choices like mutual funds, Reits, and InvITs give people a mix of chances to invest,” he added.

It is important to note that there is no change in the income tax laws’ provision under which capital gains from real estate asset sales are tax exempt if the gains are reinvested in a residential property.

Also, experts say the removal of the indexation benefit is not likely to majorly impact end-user decision making to buy new homes as this is being purchased for personal consumption. Which means investors should not lose sleep over a prolonged hit to the realty sector.

Sectoral Segmentation

What does the Budget mean for other major sectors?

Let’s take infrastructure.

The capital allocation to infra along with internal and extra-budgetary resources (IEBR) for public sector units (PSUs) stood at ₹7.4 trillion (2% more than the FY24 Budget and 6% more than FY24 revised estimates). There was no change from the interim budget.

“This is a far cry from the growth witnessed in the last two years when spending rose ~30-35% year-on-year,” InCred Equities said in a note.

In the last general election (FY20), spending declined 17% year-on-year (y-o-y). This was despite FY20 budget estimate being 8% higher than FY19 budget.

“The weak growth is in line with our expectations. Infra spending during general elections (FY10, FY15, FY20) witnessed a dip versus trendline growth. However, infra spending is robust in the year before general elections (FY14, FY19, FY24) as the government ramps up execution. We expect the strong execution in FY24 to be followed by a dip in FY25,” it added.

However, experts say taking a granular look at the numbers might throw up some opportunities.

For example, with nearly 60% of FY24’s capital outlay allocated to roads and railways, and spending on railways 51% higher than FY23 (revised estimate) and roads/highways 24% higher, these areas present significant investment opportunities, Whitespace Alpha’s Sharma said.

“Accounting for nearly 10% of total expenditure, the defence sector remains a key focus. Also, with a 30% increase in spending and accounting for 11.5% of the spending outlay, the transport sector shows promise. Education, health and social welfare have seen increases of 13%, 15%, and 18% respectively, indicating potential growth areas. With a 6% increase in allocations, the agriculture sector may also present opportunities,” he added.

That said, investors must also remember that the capex-led bull run in PSUs, railways, and capital goods sectors has been ongoing for the past 12-15 months. Which means return expectations should be tempered if you are looking to enter this red-hot segment at this juncture.

“While it might be prudent for investors to book some profits to lock in gains, there are still legs to this rally. The continued focus on capital expenditure and infrastructure development indicates that these sectors could see sustained growth in the medium to long term. Diversifying within the sectors, such as focusing on companies with strong fundamentals and growth potential, can also mitigate risks,” said Anirudh Garg, partner and fund manager at Invasset, a portfolio management service provider.

That apart, investors can also expect a further push to the nascent demand revival seen in consumer staples, durables and two-wheelers on the back of various job creation schemes.

The Budget provided a package of five schemes and initiatives to facilitate employment, skilling and other opportunities for 41 million youth over a five-year period, with a central outlay of ₹2 trillion.

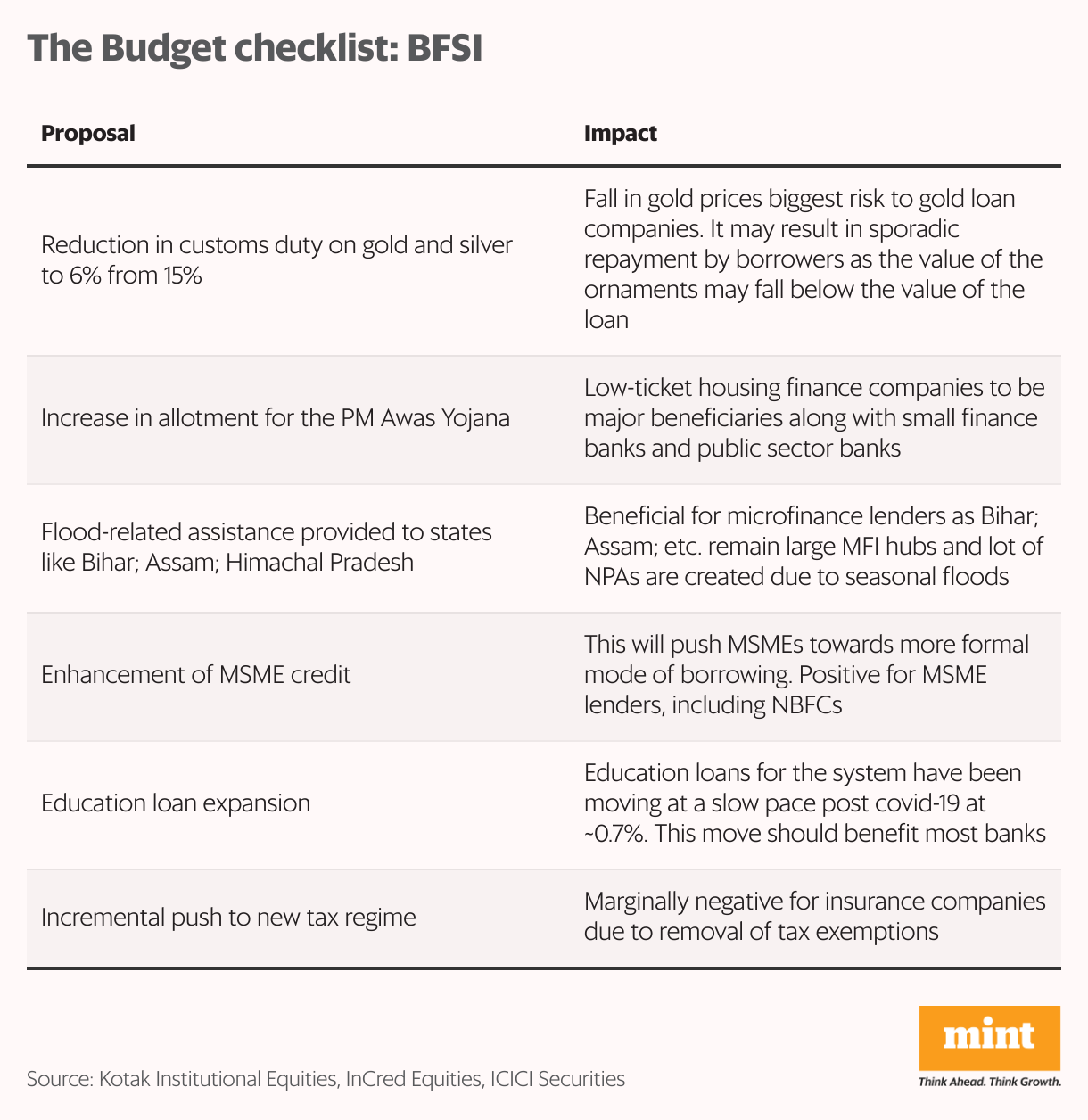

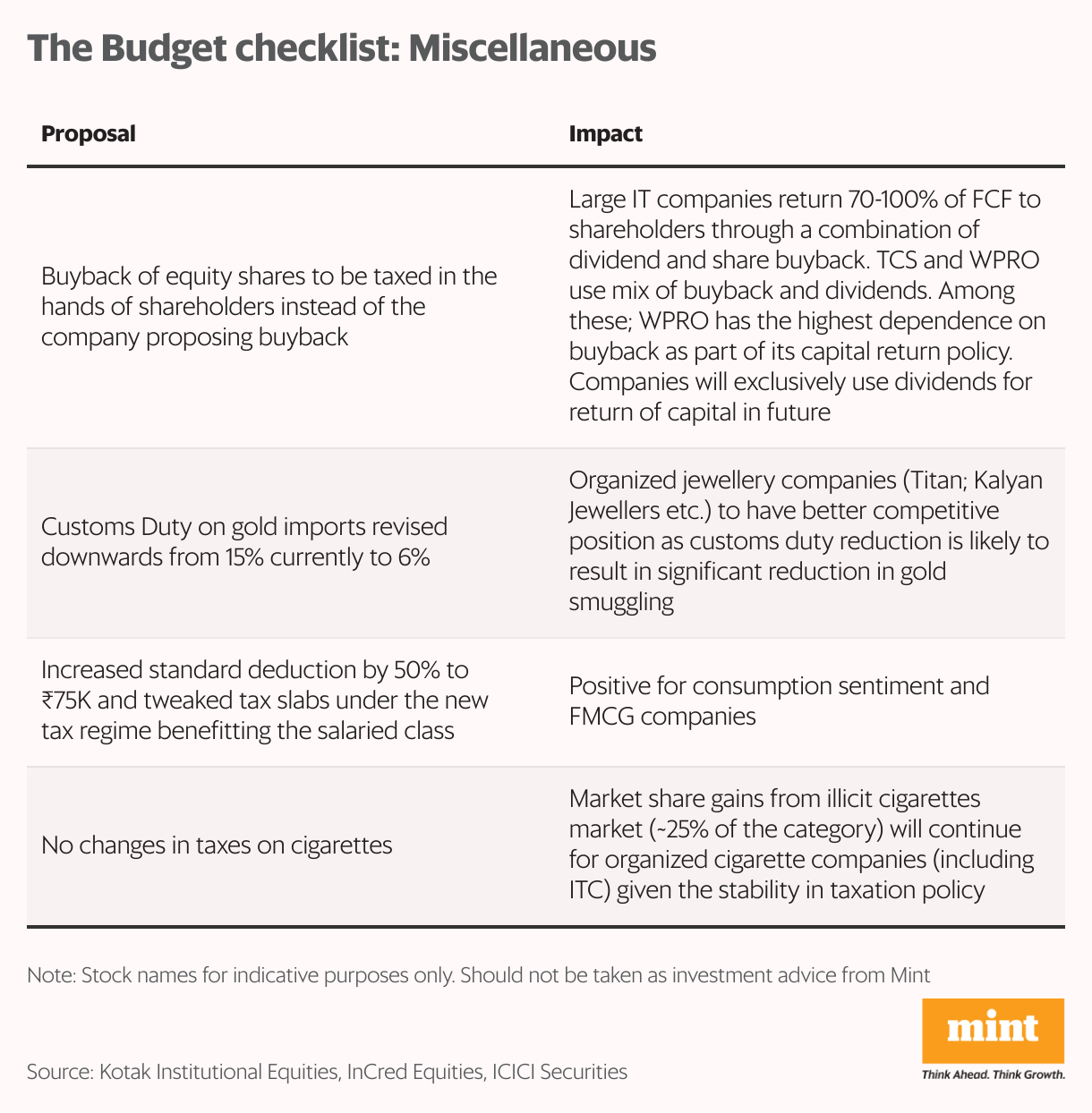

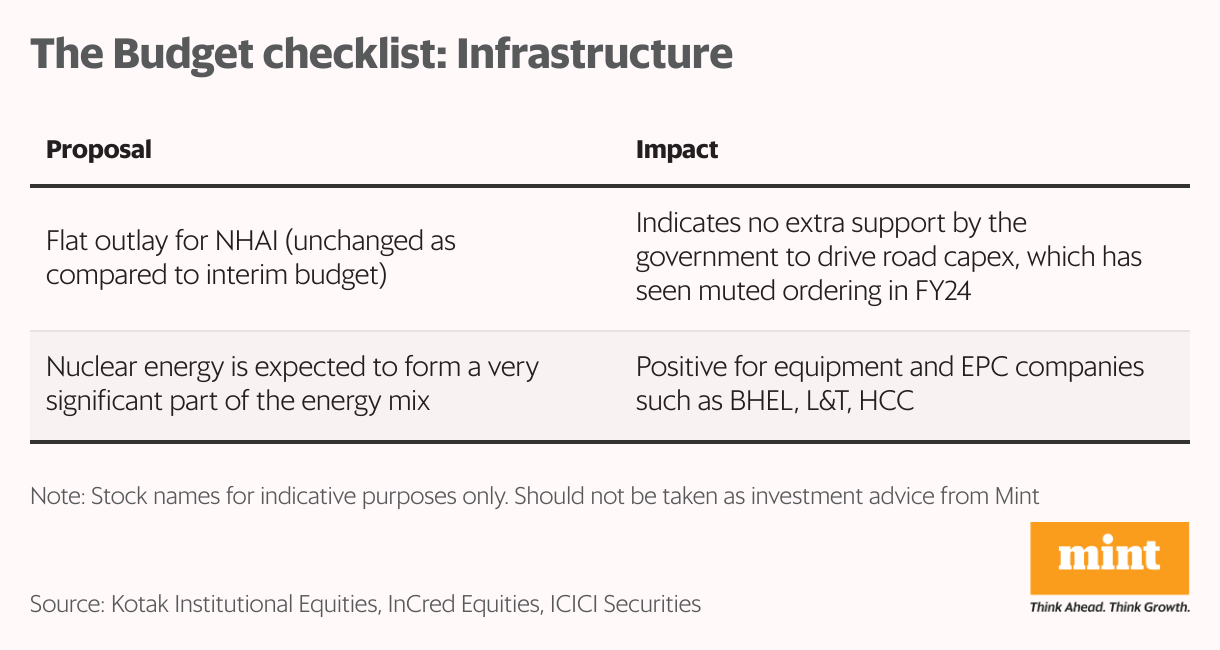

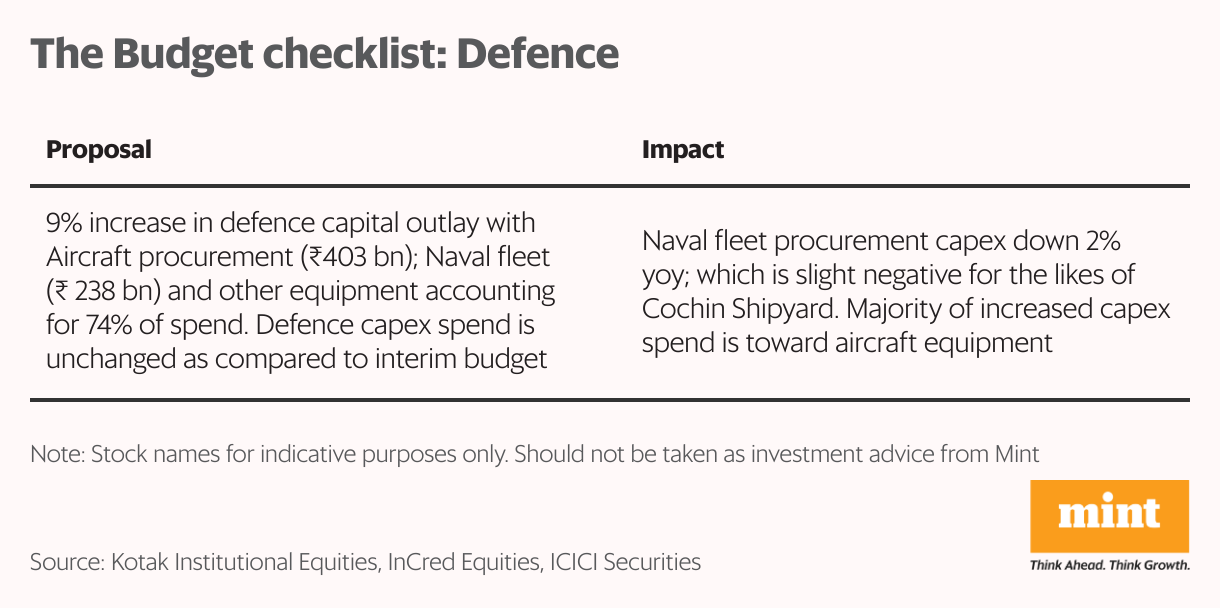

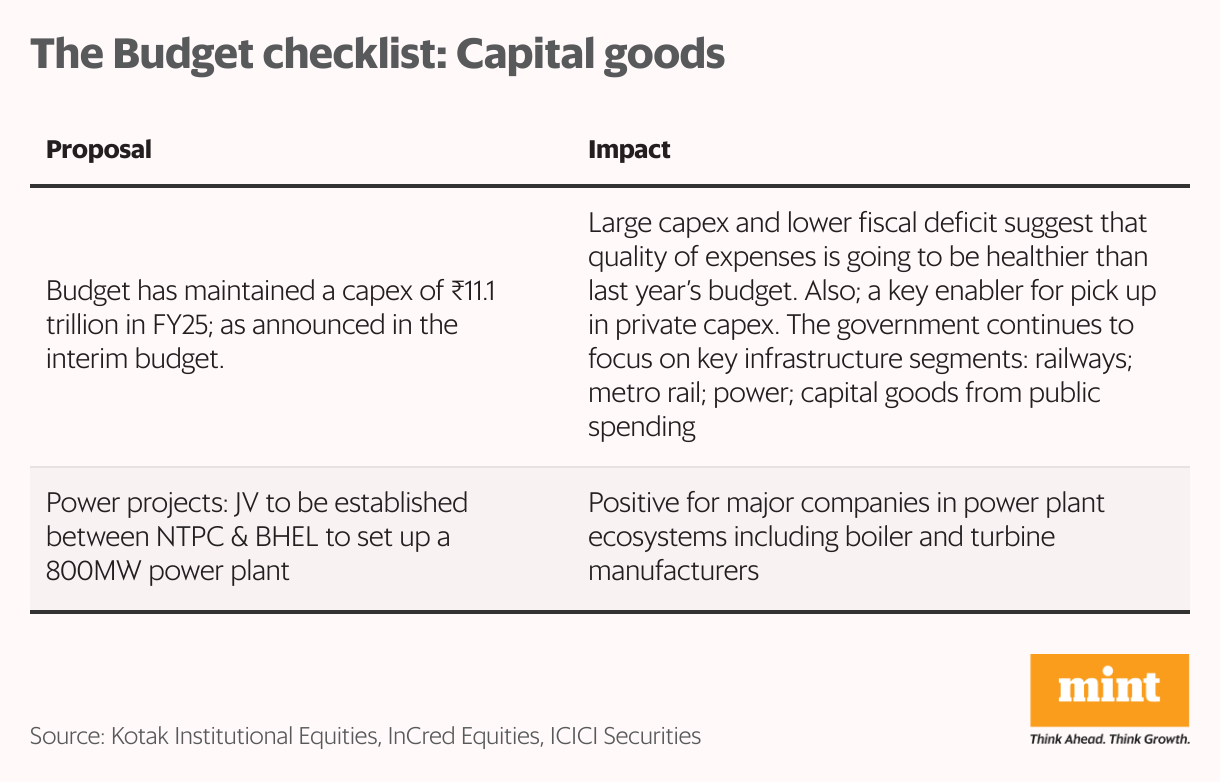

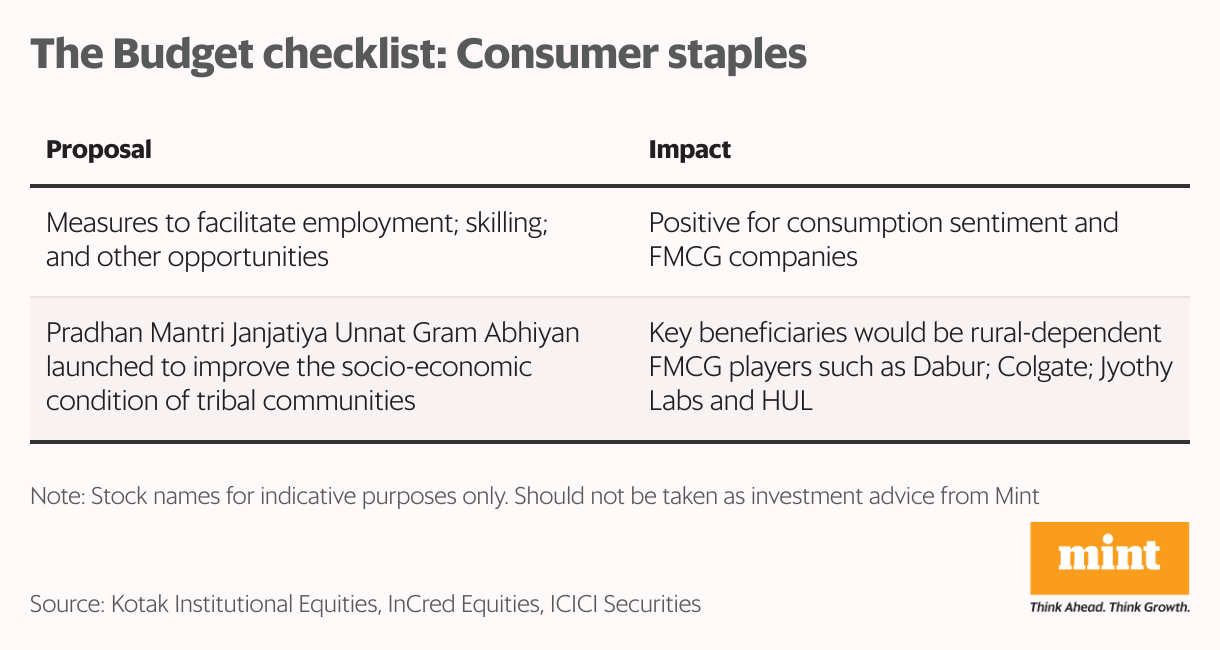

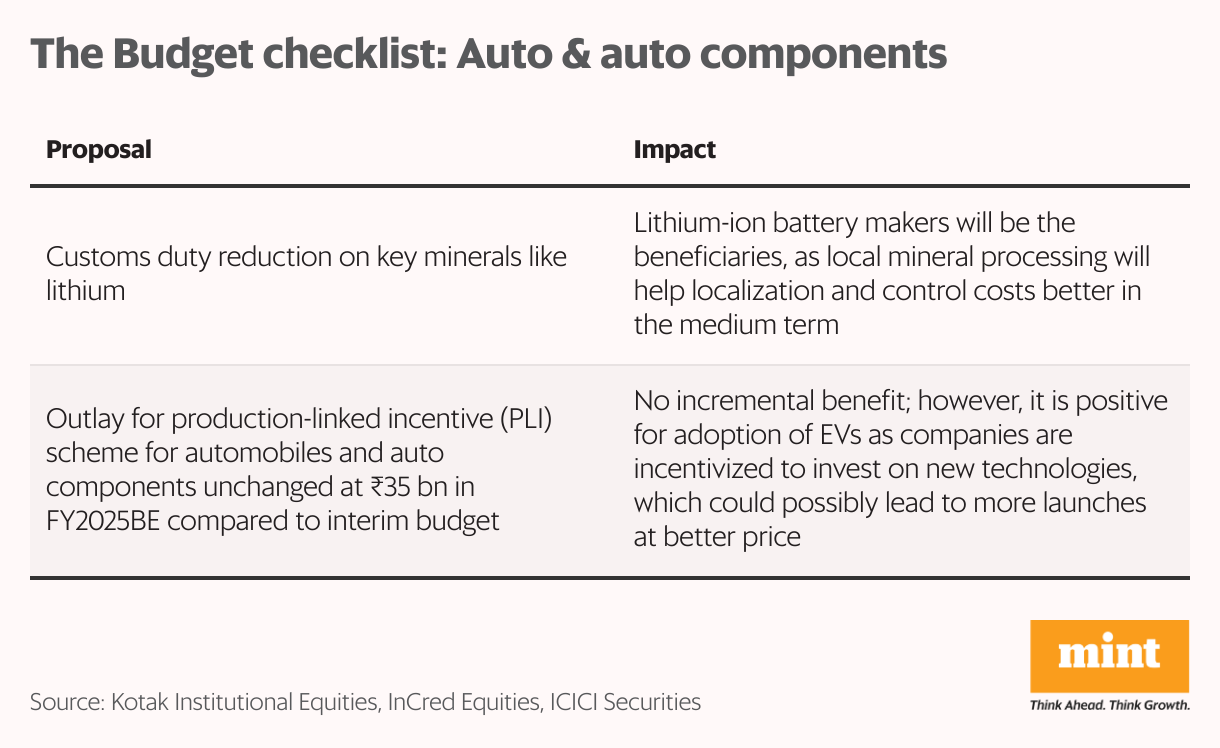

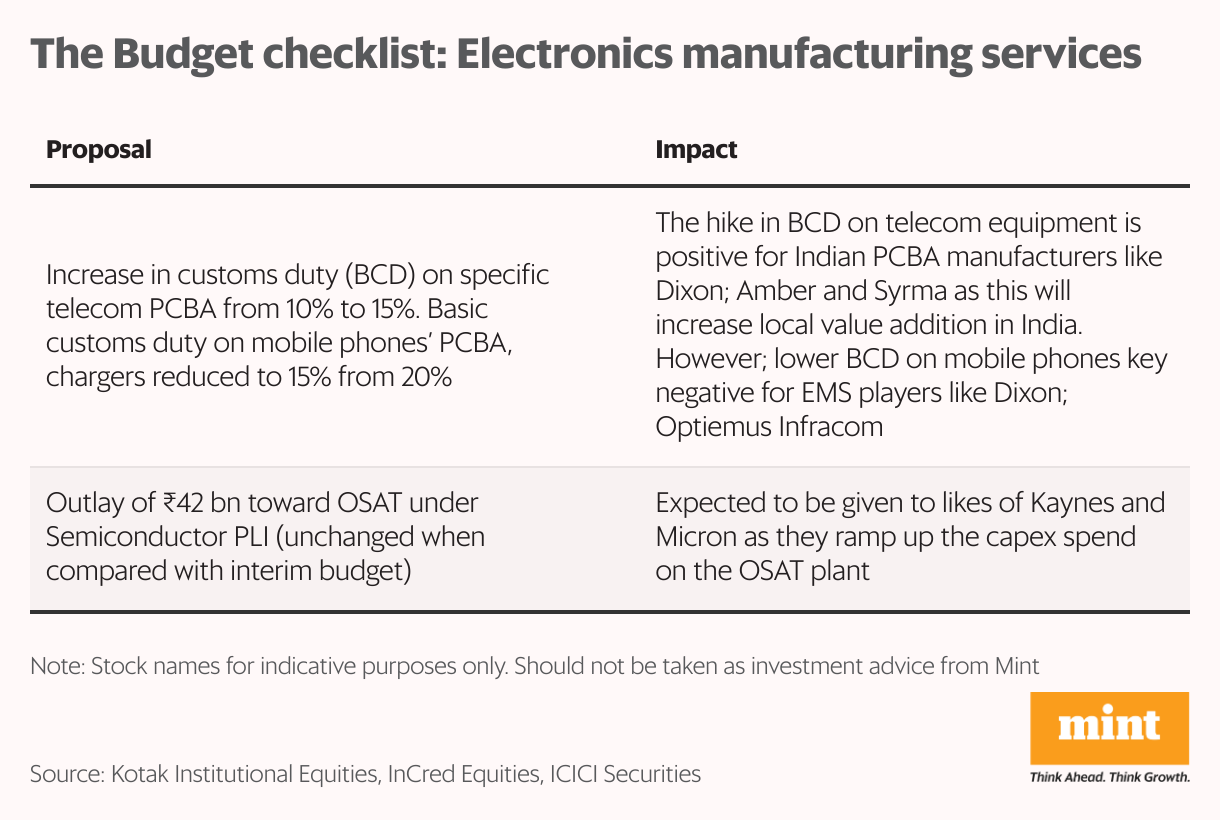

(For other sector-specific announcements, refer to the infographic).

Macro Math

A key takeaway for investors is the Budget’s focus on fiscal health.

The fiscal deficit for FY24 stands revised to 5.6% compared to the earlier budgeted estimate (BE) of 5.9%, aided by the higher-than-budgeted dividend from the Reserve Bank of India.

The fiscal deficit is budgeted at a significantly lower target of 4.9% (FY25 BE) and is expected to dip further below 4.5% by FY26.

Nominal GDP growth in FY25BE stands at 10.5%, which appears conservative given the recent upgrades to India’s GDP by the Reserve Bank of India and the International Monetary Fund.

View Full Image

Also, the buoyant growth in goods and services tax (GST) receipts as well as direct taxes indicate that the Centre should not have much trouble keeping the fiscal deficit in check.

Tax receipts (net to Centre) are expected to grow at 11% y-o-y to ₹25.8 trillion, with all its major components (corporate, personal income, GST, etc.) growing in the range of 11–13%.

“Given the declining fiscal deficit glide path, gross market borrowing for FY25 BE is likely to dip to ₹14 trillion, from ₹15.4 trillion (FY24 revised estimate). We believe declining fiscal deficit, as well as lower government borrowing in congruence, are positives for rising capex cycle, as these shall ensure government borrowing does not crowd-out bank credit to the private sector,” analysts at ICICI Securities noted.

Many market watchers were worried about a rise in populist measures in the backdrop of the Bharatiya Janata Party’s recent electoral hiccups, but the government has resisted this temptation.

For FY25, subsidies are expected to dip across the board—fertilizer subsidy at ₹1.6 trillion (-13.2% y-o-y), food subsidy at ₹2 trillion (-3.3% y-o-y) and fuel subsidy at ₹0.12 trillion (-2.6% y-o-y).

While interest payments are expected to rise 10.2% y-o-y, ‘grants in aid for the creation of capital assets’ jumped around 29% y-o-y to reach ₹3.9 trillion.

Towards Tomorrow

For many wistful market veterans, the turning point for Indian equities came in 2004, when the then finance minister P. Chidambaram abolished LTCG tax on the sale of listed shares. Instead, he levied a securities transaction tax, a small tax on the value of the purchase and sale of securities.

However, this era came to an end in 2018 when former finance minister Arun Jaitley reintroduced a 10% LTCG tax on gains exceeding ₹1 lakh, without allowing indexation benefits. The securities transaction tax too was retained.

What should be the major takeaway from this episode? Capriciousness of Indian policymaking? Perhaps, but the more important point, at least for investors, is that the benchmark Nifty today has gained over 132% in absolute terms from that period. Small- and mid-caps have climbed higher. Some individual stocks have delivered life-changing returns to patient investors.

Investing is a much bigger game than just minimizing the tax impact. Of course, tax hikes are painful, but grieving over something we cannot control is hardly the recipe for success, experts say.

Taxes might increase in the near future ormight evendecrease after a change in government.No one knows, but since everyone’sin the same boat, the only way to get an edge is toget the basics right, experts say.

“The government’s continued focus on infrastructure development indicates that these sectors could see sustained growth in the medium to long term. However, investors should also diversify within the sectors and focus on companies with strong fundamentals and growth potential,” Invasset’s Garg pointed out.

In other words, stick to the fundamentals and don’t be swayed by daily headlines in your journey towards wealth creation. These principles were as relevant during Henry Davis’ Wall Street era as they are today.