—Peter Lynch

If you are ever depressed by your stock-picking skills, here’s a quick morale booster—even the giants of the game get it wrong sometimes. Case in point: the ‘father of value investing’ himself.

In the heady days of the 1920s, an era so exuberant that it was dubbed the “Roaring Twenties”, legendary investor Benjamin Graham was grappling with a problem many of us are facing right now. How to invest in a raging bull market.

Graham, who was then managing a hedge fund, devised a simple technique—buy the most “undervalued” stock and short sell the most “overvalued” share in each major group. However, he soon learnt a timeless lesson. Individual brilliance, no matter how formidable, is no match for Mr Market.

Graham discovered that his technique did not work at all because stocks tended to move both up and down as groups, leaving virtually no room to differentiate between over- and undervalued counters.

Market fads have a far greater impact on stock price movements than we realize.

Decades later, well-known American investment consultant Charles D. Ellis, in his bookInstitutional Investing, documented this with a study showing that beyond overall market conditions, two-thirds of the price change in stock can be attributed to sectoral factors, while only one-third is due to characteristics of the individual company.

In other words, market fads have a far greater impact on stock price movements than we realize. This raises an interesting question—what would Graham make of the hottest fad on Dalal Street right now—public sector undertakings (PSUs)?

Rallying Point

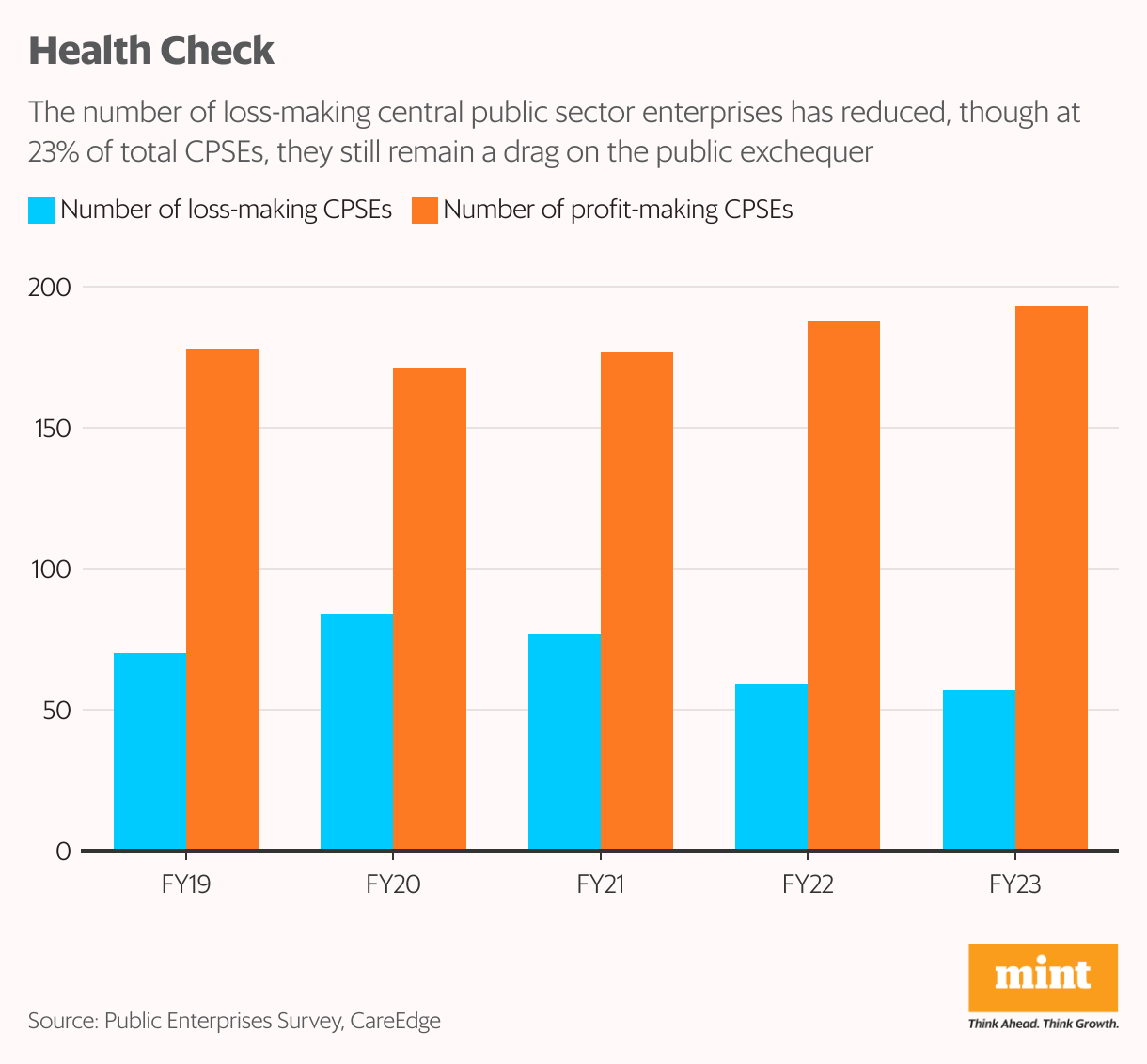

From being synonymous with institutional lethargy and inefficiency to emerging as one of the biggest wealth creators, PSUs have indeed come a long way.

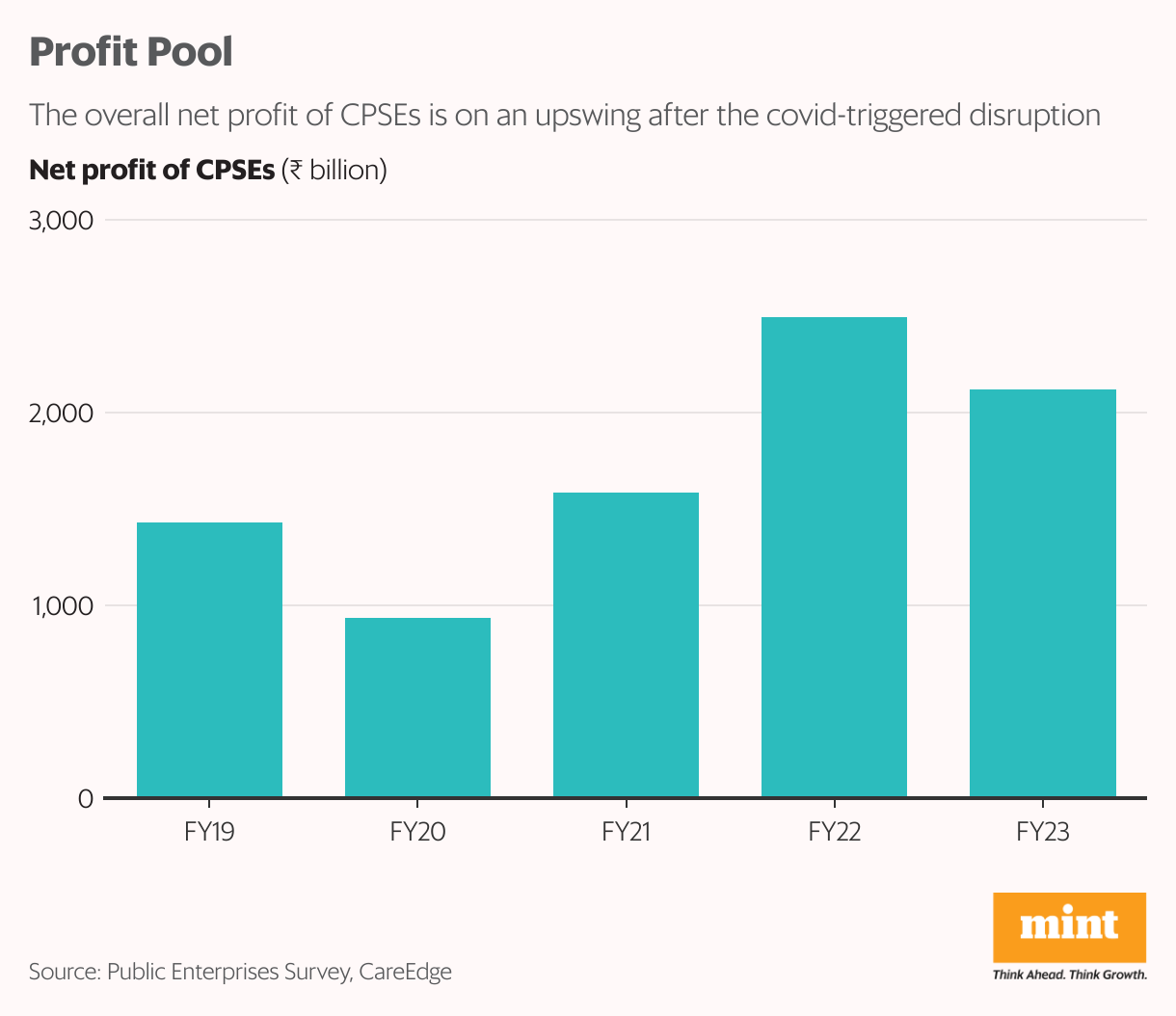

The 56 listed PSUs which are part of the BSE PSU index posted a cumulative profit of over ₹5 trillion in 2023-24, an all-time high. The profit pool of all 12 public sector banks, which till a few years ago were gasping for breath under a humongous pile of sour loans, has soared over four times in three years to a record ₹1.4 trillion.

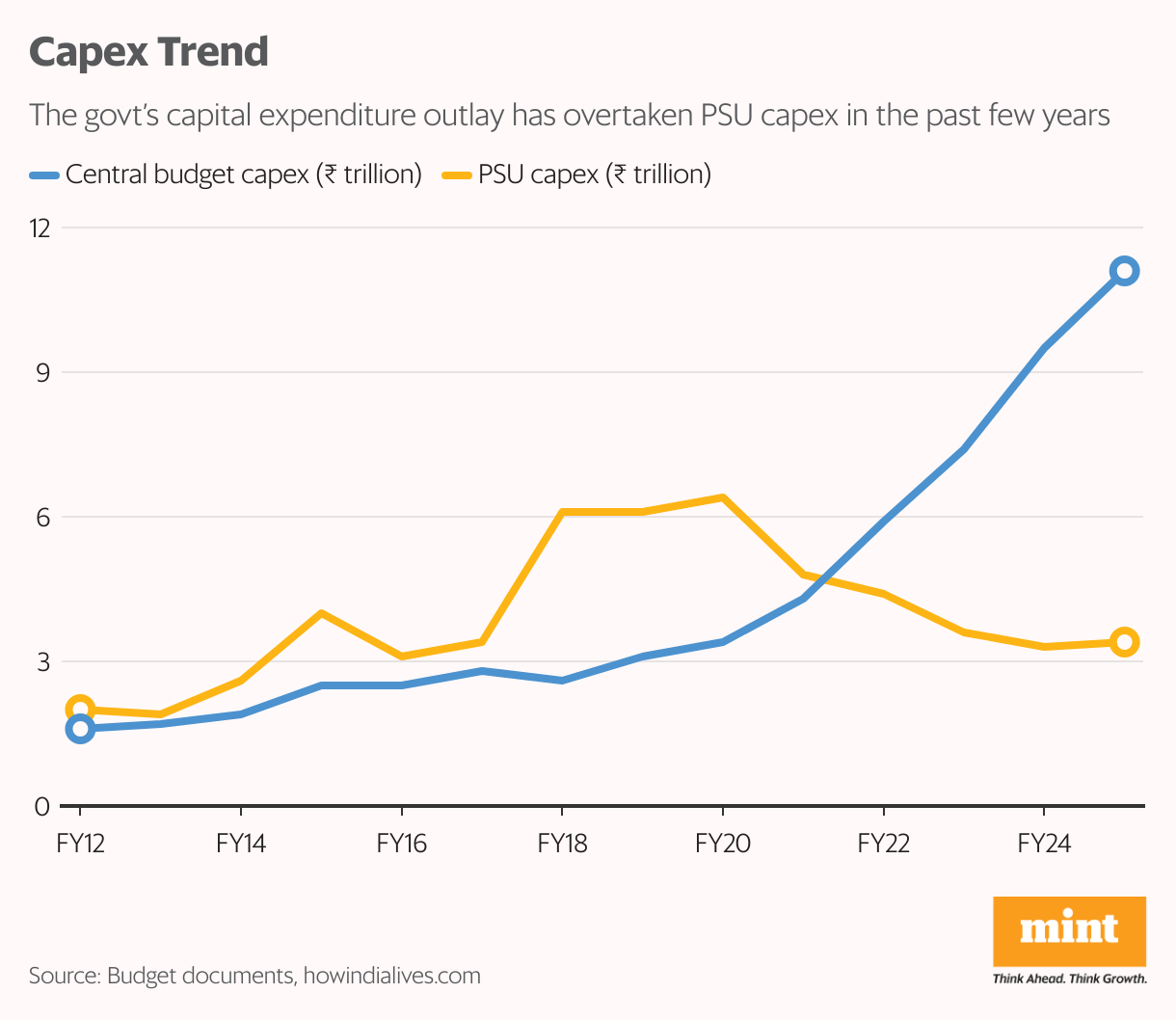

The government’s focus on revitalizing India’s infrastructure, and the concomitant increase in capital expenditure, have been the principal drivers for the change in fortunes of public sector enterprises.

The Centre’s budgeted capital expenditure, used for creating long-term assets like roads, ports, machinery, energy infrastructure etc., has soared from ₹1.9 trillion in 2013-14 to ₹11.1 trillion in 2024-25, an over 5-times increase.

At the same time, capex by public sector enterprises has risen from ₹2.6 trillion in 2013-14 to ₹3.4 trillion in 2024-25. However, PSU capex has reduced from a peak of ₹6.4 trillion in 2019-20, as budgetary capex has taken the lead in the government’s infra push.

The Centre also launched initiatives like ‘Make in India’ to give a fillip to indigenization and reduce import dependence.

Overall, the substantial jump in total capex combined with supportive policies is widely expected to spur job creation, crowd in private investments, and help achieve the government’s goal of making India a $5 trillion economy.

And the key to unleashing the animal spirits of the economy is its PSUs.

When the country’s largest lender, biggest oil producer, biggest shipbuilder, biggest coal producer, biggest electricity producer, largest insurer, biggest aerospace company and biggest steel maker are all public sector companies, it would not be an exaggeration to say that the road to prosperity passes through the portals of India’s public sector giants.

Which is something the market had realized quite some time back.

Market Mojo

View Full Image

Anyone who believes “elephants can’t dance” has clearly not passed through Dalal Street.

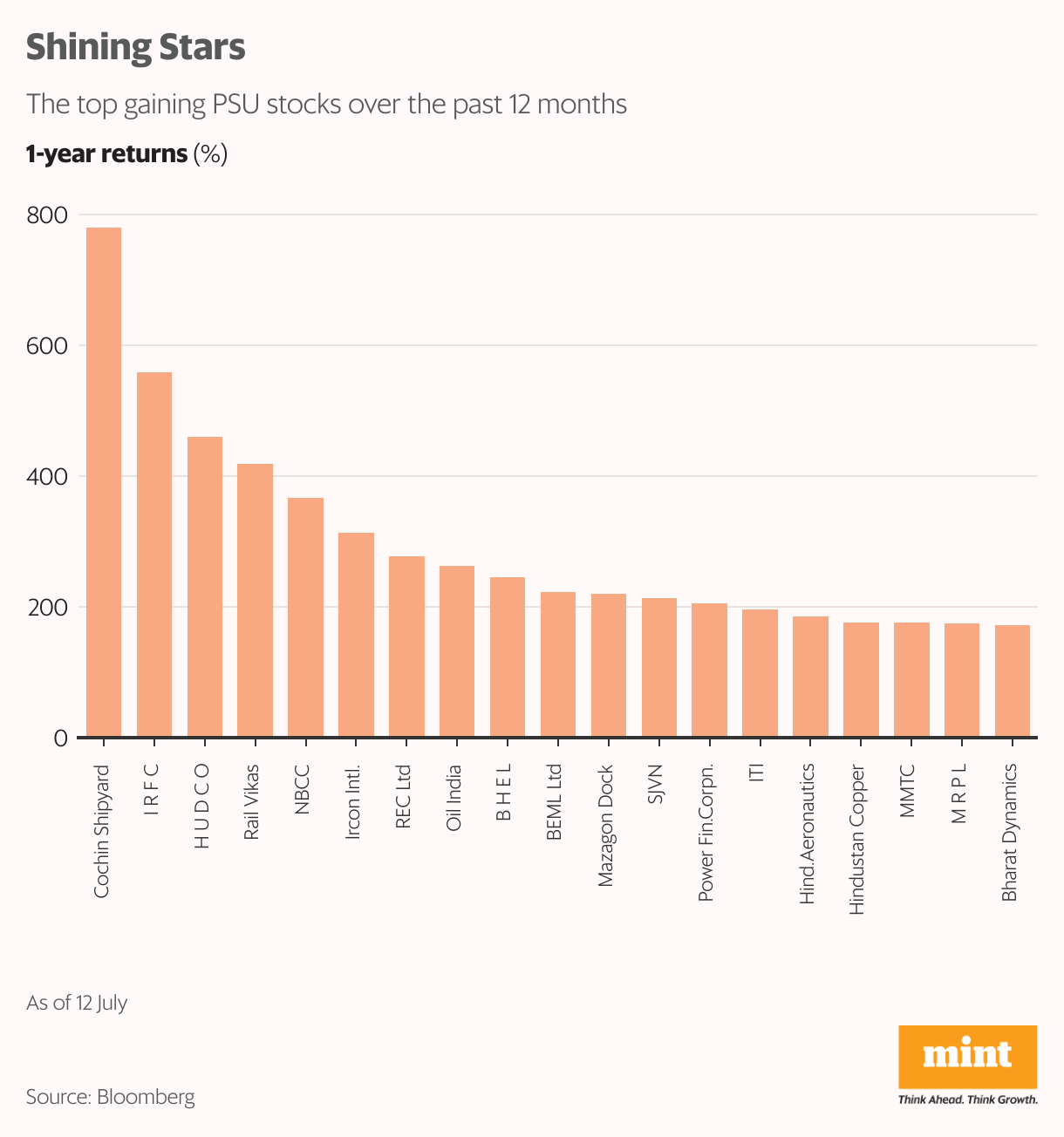

Over the past year, the market capitalization of India’s listed PSUs has climbed from $404 billion to $804 billion. The BSE PSU Index has been among the best performers during the period, delivering over 100% returns.

Some PSU names have not only overtaken small- and mid-cap companies in returns but have eclipsed even traditionally jumpy assets like cryptocurrencies. If you had invested ₹1 lakh in Cochin Shipyard Ltd a year ago, you would have a cool ₹8.32 lakh today—an astonishing 732% return.

IRFC has been the second-highest gainer in the PSU pack, climbing 553%in 12 months. Some other winners include HUDCO (up 465%), Rail Vikas Nigam (up 420%), NBCC (347%) and Ircon (287%).

“The rally of public sector units as a whole started with the launch of Atmanirbhar Bharat scheme. As these companies are leading capex-centric businesses, they become beneficiaries of this theme. The market took note of this and re-rated the shares of the PSUs. The price-to-earnings (PE) multiples expanded with the expansion of order books and earnings,” said Manish Bhandari, chief executive officer (CEO) and portfolio manager of Vallum Capital Advisors.

While the capex push has been a major trigger for PSUs’ outperformance, many investors are overlooking an equally critical factor—the market cycle.

“PSU stocks have had a good run post covid-19 and even better over the last 15 months. Some of this was warranted as they had had a decade of underperformance/range-bound stock movement. Between FY09 and FY20, the BSE PSU Index market capitalization remained flat at ₹10–11 trillion. So, some normalization was anyways due,” Harshad Borawake, head of research and fund manager, Mirae Asset Investment Managers (India), told Mint.

However, he added that at the operational level, PSUs have significantly improved their profitability as well as their capital structure, warranting a re-rating.

A re-rating is fine, but what about euphoria?

Alice in Wonderland

₹67,300 crore addition of market capitalization in the past one year.” title=”Cochin Shipyards Ltd. The company has seen ₹67,300 crore addition of market capitalization in the past one year.”>

₹67,300 crore addition of market capitalization in the past one year.” title=”Cochin Shipyards Ltd. The company has seen ₹67,300 crore addition of market capitalization in the past one year.”>View Full Image

A central characteristic of bull markets is that earnings rise in arithmetic progression, but expectations increase in geometric progression. Which is why instead of being content over the PSU index doubling in 12 months, investors are itching for even higher returns. This is creating a sector-wide asymmetry in price with respect to expected performance.

Earlier this month, Kotak Institutional Equities came out with a report highlighting this disconnect between narratives and numbers. The title of the report itself was revealing—“Do these numbers make any sense?”

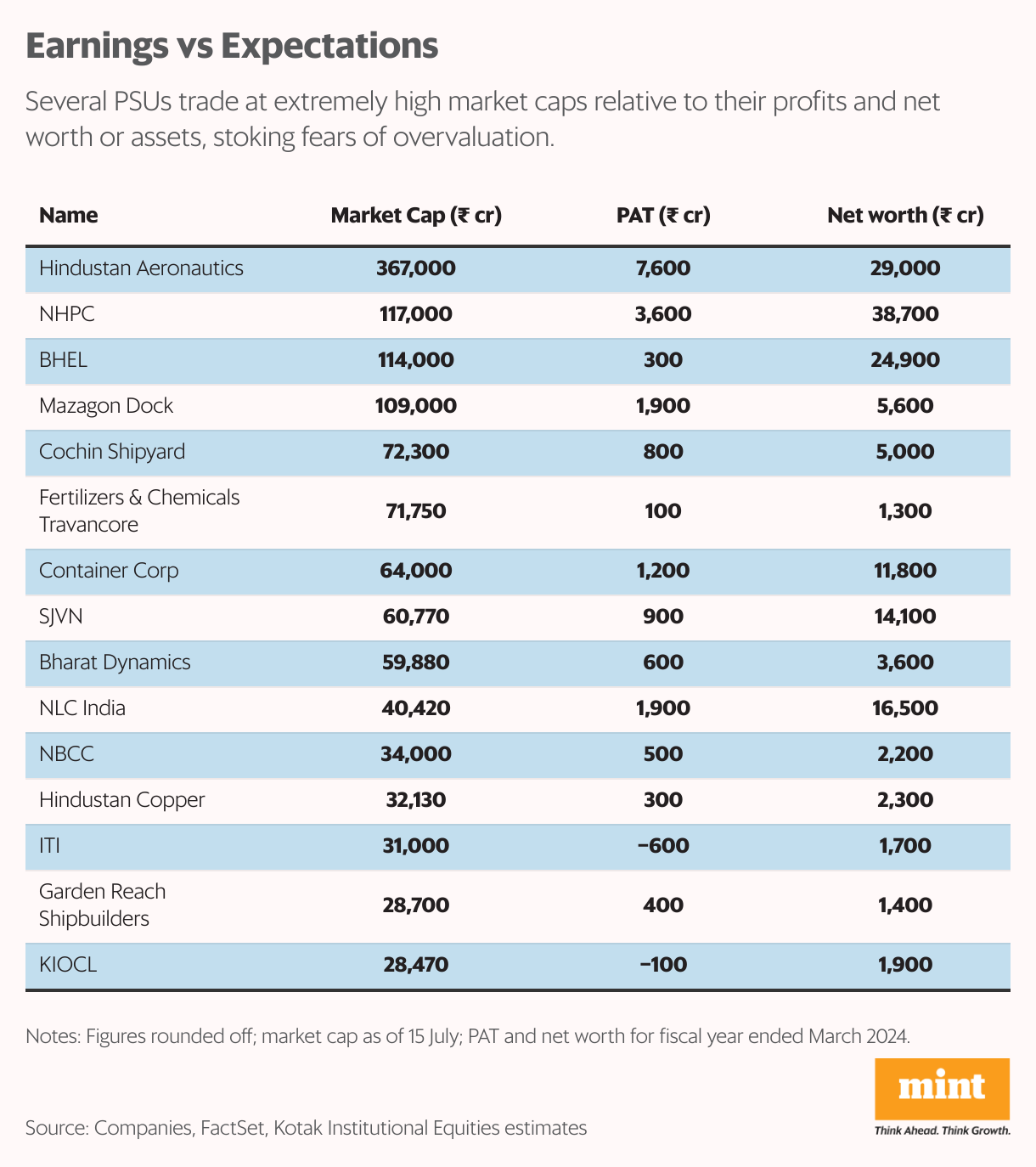

Citing the example of Bharat Heavy Electricals Limited (BHEL), it pointed out that the sharp run-up in its stock price over the past year (250%) has resulted in its market capitalization rising by a whopping ₹77,800 crore.

A central characteristic of bull markets is that earnings rise in arithmetic progression, but expectations increase in geometric progression.

This compares with a hypothetical profit pool of ₹32,000 crore to ₹64,000 crore for the entire thermal boilers, turbines and generators (BTG) equipment industry, assuming 80 gigawatt (GW) of new thermal capacity addition (in line with India’s 2031-32 target), ₹8,000 crore per GW and 5-10% net profit margin.

“The entire sector’s and BHEL’s profit opportunity would be even lower on an NPV (net present value) basis or if profit margins were to be lower. BHEL’s current market cap implies that the company will need to execute 25GW of annual thermal ordering in perpetuity, which is clearly absurd,” it said.

Or take the case of the current market darling, Cochin Shipyards Ltd. The company has seen ₹67,300 crore addition of market capitalization in the past one year, out of which ₹51,700 crore was just in the past three months.

This compares with a hypothetical profit pool of ₹5,000 crore to ₹9,000 crore, assuming that the cost of a new aircraft carrier is ₹40,000 crore– ₹50,000 crore, and 12-18% net profit margin.

“CSL (Cochin Shipyard)’s value accretion would be even lower on an NPV basis; an aircraft carrier will take years to build and deliver. CSL may not be able to participate in other opportunities. Our reverse valuation exercise implies that the company will deliver 9-13 aircraft carriers,” it noted.

For context, the US currently has 11 aircraft carriers and China has three.

The domestic brokerage house added that it does not dispute themes such as electrification of the economy, higher spending on defense etc., but is struggling with the egregious market capitalization of the beneficiary companies.

“We find the valuations of many PSU stocks to be quite bizarre when compared with their fundamentals. Most of these companies trade at very high P/E, P/B or EV/assets, and many have not seen any meaningful improvement in their fundamentals; some make losses. Some of these companies will require extraordinary assumptions and a massive turnaround in their operations (and financials) to justify their current market caps,” it noted.

Hiving Off

Ahead of the Union Budget, speculations are gathering steam over one of the strategic priorities of the government—disinvestment.

Over the past few years, divestment has been impacted by a plethora of reasons, including procedural delays, litigations by labour unions, poor market conditions, among others. The disruptions caused by covid-19 and the subsequent geopolitical volatility added to the woes, resulting in the Centre failing to meet its disinvestment target for a single year since 2019-20.

Following a robust performance in FY2017-18 to 2018-19, divestment receipts as a percentage of the budgeted target have been below the long-term average of 63% in four of the past five years.

However, the current exuberance in the market, especially in PSU stocks, presents the perfect opportunity for the Centre to rake in impressive amounts.

According to projections by CareEdge Ratings, the Centre has a huge scope for divestment worth ₹11.5 trillion in the years ahead. The analysis is based on 59 listed CPSEs and 15 listed public sector banks (PSBs) and insurance companies where the government holds more than 51% stake.

“To put things in perspective, this is a little more than twice the total divestment of ₹5.2 trillion conducted since 2014. Of this, CPSEs could contribute around ₹5 trillion, while PSBs and insurance firms could potentially add another ₹6.5 trillion,” CareEdge Ratings said.

The final decision on disinvestment, of course, will depend on the government’s fiscal position, the firms’ financial health, prevailing market conditions as well as other factors.

But analysts feel this also opens up a window of opportunity for investors.

“If the government does succeed in garnering higher proceeds from disinvestment,then investors can make maximum returns by focusing on how the government is going to use the proceeds.In our view, this will essentially be used for higher fiscal consolidation, some increase in revenue spending and capex. Essentially, this will help the overall economic growth and, to that extent, financials should perhaps benefit the most especially given that valuations in the space are also quite reasonable,” Mirae Asset’s Borawake said.

Riding the Tiger

Almost all market participants agree that some stocks are wildly overvalued right now. What else can explain Cochin Shipyard trading at a price-to-earnings (PE) multiple of 92 (compared to its 10-year average of 18.4), or Rail Vikas Nigam commanding a PE ratio of 82 (10-year average at 14)?

Following a trend or momentum might help in the short term, but only as long as everything is rising upward.

-Harshad Borawake

But this is what is so charming about bull markets—‘hot’ stocks often get ‘hotter’, making analysts and statisticians question their sanity.

“Following a trend or momentum might help in the short term, but only as long as everything is rising upward. And it is always difficult to time, hence investors should focus on the margin of safety by assessing what the current market value is factoring in terms of future earnings growth,” Borawake said.

“For PSUs, the normalization trade, in our view, has largely played out and to that extent, the low hanging fruits have been plucked. Hereon, demand/orderbook and earnings growth need to sustain to have a smooth ride,” he added.

The market goes through micro-bubbles, like IT in 1999, retail in 2008, pharmaceuticals in 2014, NBFCs in 2019, and chemicals in 2021.

-Manish Bhandari

They say pessimists sound smart, but optimists make money. Of course, the line between optimism and delusion is a thin one, but this can be hard to grasp for many gung-ho investors, especially the post-covid ones who have not experienced market cycles.

“The market goes through micro-bubbles, like IT in 1999, retail in 2008, pharmaceuticals in 2014, NBFCs in 2019, and chemicals in 2021. This is caused by euphoria for a particular sector. Today, the PSU pack is witnessing similar euphoria,” Vallum Capital’s Bhandari said.

As we saw in Graham’s example at the beginning, during intense market cycles, there’s little to differentiate between stocks belonging to the same sector. Which means stock picking at this juncture can be a fool’s endeavor.

The question investors need to ask, therefore, is not whether to invest in PSUs or not, but whether they are short-term momentum chasers or long-term participants.

If you are in the second group, experts say the bubble-territory valuations should make you pause and reflect. The rest can keep riding the tiger till the rally lasts.